- December 23, 2024

-

-

Loading

Loading

Symbols often say it all.

After the town of Longboat Key and the International Firefighters Association Local 2546 completed their negotiations last week, lo and behold, there was a cigar sitting on a table on the firehouse porch.

Probably for a few celebratory puffs. For them, not taxpayers.

If you examine the results of the latest round of union negotiations, you can conclude the union secured a better deal for its members than did town negotiators for taxpayers.

Both sides — the town administration and firefighters — are calling the contract a win-win. But certainly it’s a win for the firefighters. They got, the town gave.

To start with, the town already had a good deal. In the previous contract negotiations, the firefighters union pleaded to participate in the state’s Florida Retirement System, an expensive defined benefit plan. The town said OK, but the town said it would agree as long as it could put a cap on how much taxpayers would have to pay into the state system.

The town agreed to pay half of each firefighter’s required annual contribution — up to 13% of the required amount — above the 3% that every participant is required to contribute. At present, the state is requiring a contribution of 25.04% of each employee’s pay. For the town, that’s 11.02%.

That’s a lot, but at least it’s capped. Who knows? Some day the state system may require a 28% or 30% payment, but the town’s share would go no higher than 13%.

Moreover, in the previous contract, the town managed to eliminate the firefighters’ “step plan,” the dreaded system that simply increases employees’ pay based on longevity.

But in this year’s talks, the union decided it didn’t like what it had negotiated in the previous contract.

The town pretty much caved.

Rather than stick to what the town had — which, by the way, was considered a model for other Florida municipalities — in the newly ratified contract, the town gave firefighters what they wanted.

For starters, the step plan is back. Firefighters will receive automatic rases in 2017 and 2018, once again rewarding longevity, not merit.

But the bigger town giveaway was the elimination of the 50-50 sharing of the FRS’ required annual payments. Firefighters will continue to pay the first 3% of the required contribution to their pensions, as they did before, but the town would then contribute the remainder — no matter how high or low it might be. In other words, this contract would take the town back to what amounts to another expensive, open-ended defined benefit plan for firefighters.

When you look at the salary schedules under this contract, firefighters’ base pay will fall, but their overall compensation would rise — thanks to the town’s higher contributions to their pension plans.

To be sure: Longboat Key’s firefighters and paramedics do a terrific job when called to duty and are a crucial asset to Longboaters’ safety.

But we continue to maintain the International Association of Firefighters is a monopoly cartel. The union leaders for each local constantly leverage each other’s benefits as a way to secure higher pay and benefits.

When the Town Commission votes Monday whether to accept this contract, we urge commissioners to have the courage to reject this new contract. The town learned a hard lesson once with an open-ended pension plan. Don’t repeat the mistake.

Town’s rising debt: Generational updates

The more you read about Longboat Key’s fast-rising debt burden, the more it begins to sound alarming.

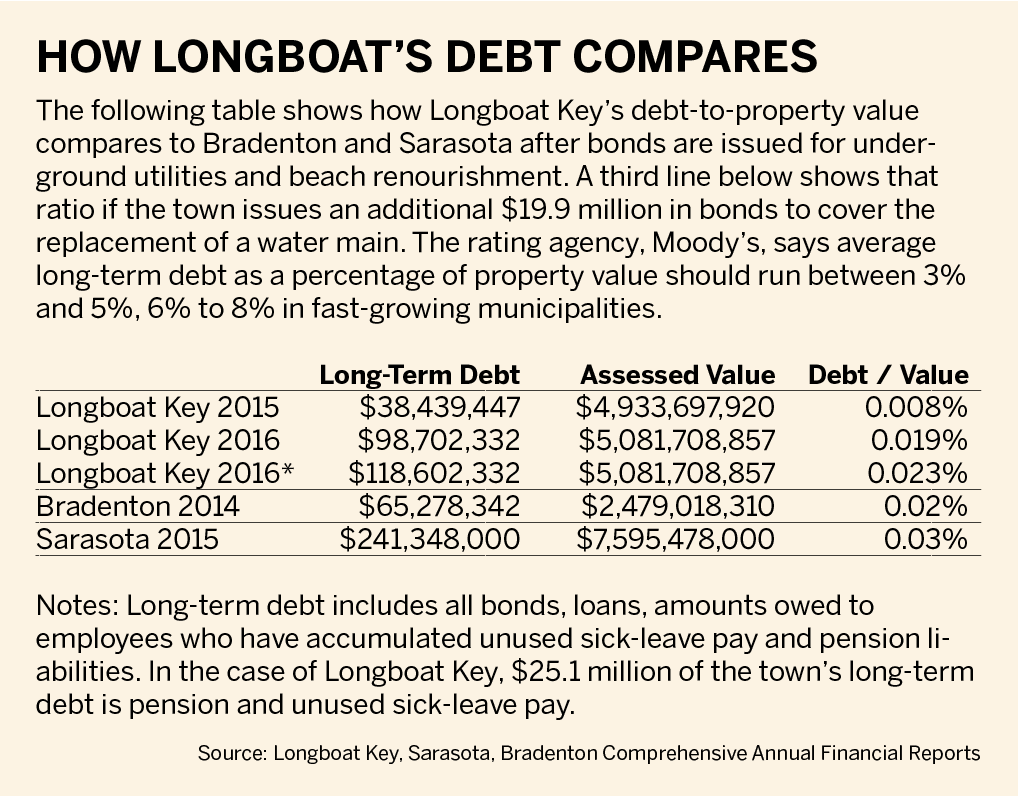

By the time all of the bonds are issued to complete the conversion to underground utility lines and this spring’s beach renourishment, Longboat Key’s long-term debt will have risen 156% from its current levels.

And it may rise even higher. If it turns out the town must also replace an underwater wastewater pipe, estimated at $19.9 million, that would push the increase in the town’s long-term debt up 208% — from $38.4 million now to $118.6 million.

These are staggering increases and big dollars for a town whose annual budget is $16 million.

But stay calm. Longboat taxpayers should not leap to visions of Detroit, Jefferson County, Ala. (Birmingham) or Stockton, Calif. — all of which have declared bankruptcy because of too much debt. Longboat Key is a long, long, long way from that, thanks to the extraordinary value of its sand and properties — and the town’s historical fiscal conservatism.

As the accompanying table shows, all of the town’s combined long-term debt — including unfunded pension liabilities of $25 million — is less than 1% of the total assessed value of Longboat Key’s property. And that is well below what Moody’s, the fiscal rating agency, considers an average ratio of long-term debt-to-property value — 3% to 5%.

On top of that, consider that Longboat’s millage rate is only 2.13 mills, well below Florida’s legal limit of 10 mills for municipalities.

In other words, the town could take on far more debt even before it reaches average debt levels.

That’s the good news. As much as it may appear the town is heading toward the national model of borrowing beyond its means to fund the town’s infrastructure projects (beaches, underground utilities and new water mains), the town actually remains fiscally conservative compared to Moody’s norms.

But of course, these necessary infrastructure upgrades and increases in borrowing still come at a price. That’s the bad news.

The town recently sent out its notice of assessments for the Gulf of Mexico Drive underground utility project. For those who choose to make the annual payment, it could add anywhere from $153 to $287 a year to what property owners pay the town in 2017.

And assuming the neighborhood underground utility project is validated later this year, Longboat property owners will see another assessment in 2018, ranging from $474 to $618 per year per property.

On top of these assessments, this year’s beach renourishment projects will take another $9 million to $11 million in borrowing. That, too, will push up the town’s beach millage rates. Town Manager David Bullock also reported in a preliminary budget that if the town determines it needs to replace that underwater wastewater pipeline, the town could borrow up to $13 million more on a 2009 bond and would likely increase user rates or more borrowing to generate an additional $5.9 million that will be needed over the next five years. Bullock is expected to present his estimates for all of this capital funding at a June 27 commission workshop.

Suffice it to say Longboat Key property owners are going to see the town’s property taxes and assessments go up the next few years — even if the Town Commission manages to keep its base millage rate where it is — at 2.13 mills, the level Bullock is proposing for 2016-2017.

No doubt we have overwhelmed you with numbers. Specifically what you will pay in property taxes won’t be known until the end of the summer, when the Town Commission and Sarasota and Manatee school boards and county commissions definitively set their tax rates.

But perhaps the larger takeaways here are:

1) Longboat Key is undergoing generational infrastructure updating. The water pipes and utility lines have lived their useful life. The residents who have lived here for the past 20 years have benefited from investments made 30 or more years ago. But now they are paying the initial costs for the next 50 years of infrastructure.

2) Longboat’s beach — the foundation of the island’s value — will remain forever an expensive proposition. The quest for more efficient, less costly ways to maintain the beach should never end.

3) It’s worth having the discussion: Knowing what capital projects are in store, how best should they be financed — primarily via bonded borrowing? Taxation that sets aside designated amounts each year? A combination of the two?

It must be June. Tax rates and local government spending are coming. front and center.